Gym and Fitness Business Accounting & Reporting Best Practices

Table of Contents

Keep Personal and Business Expenses Separate

It can be very tempting for a small business owner to just use their business credit or debit card to do personal buying, especially if the owner isn’t on payroll. Not receiving a regular payroll deposit means you have to do regular withdrawals or transfers from your business account to your personal, which can be easy to forget. When you are at the store and remember you have very little in your personal account, it’s easier to just pull out your company card and use it. But mixing personal and business expenses is never a good idea.

For one thing, it’s easy to forget which were personal and which were business when you get to your bookkeeping. There’s a chance it will go on your income statement as a business expense. If your company is ever audited and those personal expenses are found out, that becomes a tax fraud problem for you.

It also distorts your business’s actual performance. Any KPI’s with those costs included will be incorrect, which can give you, your partners, investors, or lenders a skewed picture of the company.

Also, if those stakeholders catch on that you’re mixing personal and business, they are much less likely to trust you or want to do business with you.

Monitor and Control Expenses

While we’re on the subject of expenses, let’s talk about tracking and control. Everyone knows to make sure all costs get recorded, but are you closely monitoring and analyzing your expenses?

Did expenses suddenly spike one month? If so, why? Are there any unusual costs that could indicate employee misuse of funds? Do you have a good system for detecting duplicate invoices or payments? Do you require an authorization before someone can make a large purchase? Are your vendors charging you more for the same products or services? If so, is it warranted or possibly a mistake? Are there any costs that could be cut out or reduced?

These are just a few of the things you should be asking yourself when you look at your costs. Some bookkeeping programs come with a built in dashboard, or a selection of charts, graphs, and KPI’s that can make spotting trends and problems easier. Or you can hire an accountant that’s able to provide customizable visualizations for you. A good accountant should also be able to provide insights to you, spot trends, and highlight issues.

Keep Receipts and Source Documents

Storing receipts and invoices can take up room and be a hassle. Not surprisingly, some business owners choose to record them and then trash them. But that’s not a good idea. It’s always a good practice to keep a copy. If you are ever audited or need to research something in the past, you will be glad that you have them.

Thankfully, more and more places are sending invoices through email, so that there’s not so much paper to deal with. And more stores are offering to email receipts instead of printing them.

You can store digital versions in an email folder or on your business server. Many accounting programs also allow you to attach electronic copies of documents to transactions.

If you don’t want to keep paper receipts or invoices, you can either get a scanner or take a picture of them. Programs like QuickBooks allow you to email receipt pics directly to your account. Just make sure you have an electronic copy of them before they go in the trash.

Enter Depreciation Monthly

A lot of small businesses only enter depreciation expense for fixed assets at the end of the year. They wait and let their tax accountant tell them what to enter. The problem is, you might have one big depreciation expense entry in December that skews reporting.

For instance, if you buy $75k in exercise equipment in February, there will be no expense showing for it until December. And due to special tax depreciation rules, like section 179 and bonus depreciation, that equipment might be fully depreciated in the year purchased. So, you might have a whopping $75k expense in December that makes it look like you experienced a loss that month.

It’s better to enter deprecation expense monthly so that the cost of it is spread out over the course of the year or over multiple years. You can then true it up to taxes at the end of the year if you want.

Equipment Accounting

For gyms, other than the building itself, exercise equipment is the most expensive thing you own. And over time, equipment can break, become outdated, or just not get used by your members.

When equipment is sold, impaired, or thrown out, it requires special accounting treatment. The technical nature of it can make it easy to screw up your books.

When you sell an asset, you have to factor in the effect of depreciation and whether or not you end up with a gain or a loss. Let’s say you bought an elliptical machine for $5k. You depreciated $3k of it. You then sold the machine for $1,500 because you wanted to buy a more up to date model.

Purchased For = 5,000

Depreciation = 3,000

Net Book Value = 2,000

Sold For = 1,500

Gain/Loss = -500

The accounting entry would look like this:

| Debit | Credit | |

| Loss on Asset Disposal | 500 | |

| Accumulated Depreciation | 3,000 | |

| Cash | 1,500 | |

| Elliptical Machine | 5,000 |

If you just threw the machine away because it wasn’t usable to anybody, the entry would look like this:

Purchased For = 5,000

Depreciation = 3,000

Net Book Value = 2,000

Gain/Loss = -2,000

| Debit | Credit | |

| Loss on Asset Disposal | 2,000 | |

| Accumulated Depreciation | 3,000 | |

| Elliptical Machine | 5,000 |

Impairment occurs when an item has lost some of its value but hasn’t yet been disposed of. It’s a way of recognizing the decline in market value on your books before you do anything with it. This is a tricky one, however, because for tax purposes, you can usually only claim a loss deduction on an asset that has been sold, abandoned, or thrown away.

While GAAP accounting standards allow for it, in practice most businesses don’t bother with impairment entries because of the inaccurate nature of estimating fair market value and the complications that arise from having to keep impairment entries separate from tax reporting.

My advice is that unless you have an accountant well versed in impairments and you are confident in your market value estimates, don’t bother with impairment entries. Wait until you sell or dispose of the equipment.

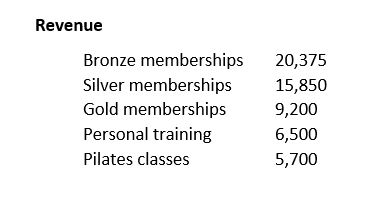

Track Revenue Streams Separately

Many fitness companies, like gyms, have different revenue streams such as various membership levels, classes, personal training, and even merchandise sales. The mistake some make is placing them all into one bucket on their profit and loss statement.

Having separate accounts on your general ledger gives you far better visibility into your business and allows for more profitability analysis.

So, for instance, instead of having just one sales account at the top of your income statement, you should break revenue into multiple accounts based on the source.

Look At Profitability Centers

Much like how you shouldn’t track income all in one account, profit doesn’t have to be in one bucket either.

When you track revenue streams separately, it opens up the possibility of treating each segment as a profitability center. That means you can allocate expenses to the revenue segments and see how much profit each is providing.

Sometimes owners are shocked to learn that what they thought was a profitable income stream was actually barely making money or even losing money once they start looking at individual profit.

Multi-Location Accounting

In the same vein, if you own multiple locations, don’t just track them all together. Many accounting programs have location or class fields in which to differentiate transactions for each branch. Many also have location specific reports built in.

Revenue Recognition

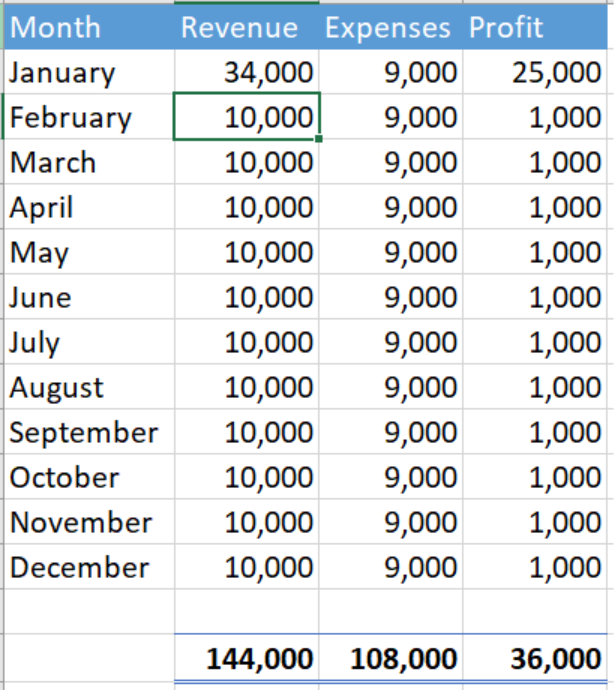

Small physical fitness and training related businesses often file their taxes on a cash basis. Thus, a lot choose to keep their books on a cash or modified cash basis as well. While cash basis bookkeeping can be okay for some businesses, it can distort earnings for others, such as those that receive advance money for services.

Some fitness centers encourage members to pay in advance through discounts or other incentives. It accelerates cash for them and cuts down on the number of billings that have to be sent out.

The problem is, if you record all of the money in the month received, it can throw things off the rest of the year.

Let’s look at an example. You receive $24,000 in membership dues in January from several of your long-term patrons. The 24k is an entire year worth of dues for those members. Let’s say you receive another $10,000 from members that chose monthly billing. And for the sake of simplicity, let’s say that the rest of the year, you receive about 10k a month for dues and that costs run about 9k a month.

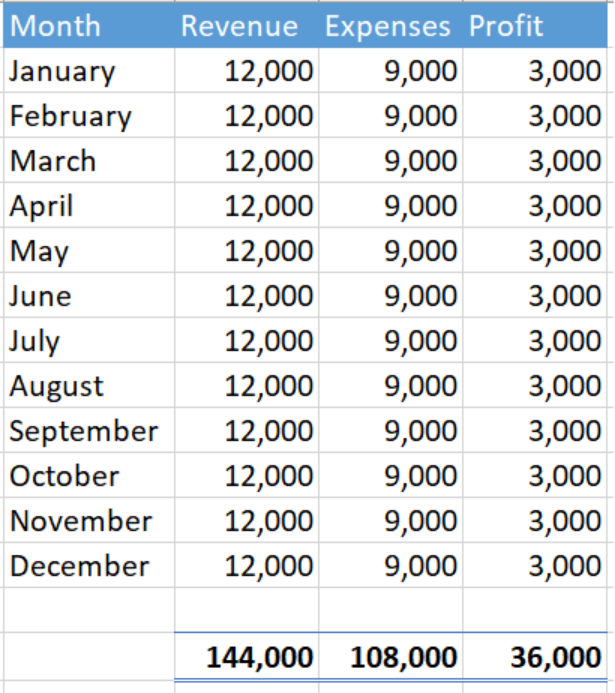

If we record all 34,000 received in January as income, the year looks pretty lopsided. We know that the 24k in advance dues is for the entire year. So, why only show it in one month? Accounting standards say that you should allocate or amortize advance income over the course of the service period. So, if your business has an obligation to provide access or services for 12 months, amortizing 2,000 a month would evenly distribute that 24k over the course of the year.

This looks much better. We have the same totals but the months are evened out. We can now analyze and compare months accurately.

You may worry that keeping your books this way will make it hard to provide cash basis statements to your tax accountant. But most accounting programs are able to automatically convert your books to cash basis when needed.

Utilize Recurring Billing

If your gym management software or bookkeeping program has a recurring billing feature, it can save you lots of time. It enables you to schedule and automatically send out monthly invoices and payment requests, cutting down on manual work. Better yet, if you have your members’ payment info on file, you can simply do automatic deductions from their account each month. Many fitness management programs and payment processors support this.

Credit Cards Should Be On Your Balance Sheet

A lot of businesses don’t have a credit card liability account on the books. They just enter all the expenses off their statement once they go to pay their balance. But a credit card is a source of financing much like a loan is, and thus, what you owe should be accounted for on your balance sheet.

As you make purchases with your credit card throughout the month, you should be recognizing them as expenses and as a liability. QuickBooks and similar programs have a built in screen specifically for credit card entries that can help you take those amounts to the correct accounts.

Reconcile All Accounts

Most small businesses at least reconcile their bank account(s), but many ignore their other balance sheet accounts such as loans payable, fixed assets and accumulated depreciation, credit card accounts, payroll liabilities, accounts payable, accounts receivable, etc.

Every account on your balance sheet should be reconciled each month. Reconciliation is a way for you to spot errors in accounts and make them right. In other words, it’s a quality control procedure. When you don’t reconcile accounts, errors can accumulate and throw off account balances significantly.

If you’re not comfortable with reconciliations, seek out an accountant to do them for you. Even if you prefer to do your own bookkeeping, accounting services like AccountAlytix can do your reconciliations and other end of month tasks for you, advise you, and provide customizable reports.

The Importance of Having a Budget

A budget can be both a control mechanism and a performance gauge. Budgets allow you to set performance goals and spending limits. For example, if you would like your salespeople to increase revenue by 15% in the coming year, you can put that 15% increase into the budgeted income total. Or if you would like to keep operating costs at a certain threshold, you can enter those limits on your expense lines.

You can then compare actual results to your budget each month, see where the differences are, find out if they are favorable or unfavorable, investigate the reasons behind the differences, and put together a strategy to correct problem areas and better the company’s performance going forward. It also allows you to hold managers accountable, identify cash shortfalls, allocate resources more effectively, and adjust future plans.

Pay Attention to Your KPI’s

KPI’s can serve as a goal setting and control device much like a budget, but instead of focusing on individual accounts on your financial statements, KPI metrics allow you to dig underneath the numbers to find out what they mean. They enable you to track your company’s progress, set targets or goals to hit, spot issues and trends, make changes, and adapt plans and strategies.

There are a number of different key performance indicators that fitness businesses should be tracking closely. Below are some of the most relevant ones. These metrics can be applied to various functional areas or departments, such as sales, front desk, trainers, class instructors, and operations management, to judge performance.

- Sales growth rate

- Revenue per member

- Revenue per training session or class

- Member retention rate

- Utilization rate for classes

- Average class or training program attendance

- New member sign ups

- Membership growth rate

- Churn rate or membership cancellations

- Marketing channel performance

- Cost per acquisition

- Conversion rate

- How many leads convert to paying members, class or training participants, etc.

- Customer satisfaction – feedback and reviews

- Profit margin

- EBITDA